Rules of Origin

From 1 January 2021, companies have had to demonstrate the originating status of goods traded with the European Union (EU) in order for these to be entitled to preferential treatment under the Trade and Cooperation Agreement (TCA) between the UK and the EU. Goods not meeting origin requirements, and therefore not deemed to be of UK or EU origin, will not qualify for preferential treatment and will be liable to customs duties (tariffs). In order for a business to benefit from preferential tariffs, agreed in the UK-EU TCA, importing into the UK or EU, they will need to claim preference on their customs declaration and declare they hold proof that the goods meet the Rules of Origin.

What are Rules of Origin?

Rules of Origin (ROO) allows an importing country to identify and classify the origin of a product. It is a straightforward process when the product is produced in a single country. Given modern global supply chains comprising of components and processes undertaken in numerous states, the application of this ROO can be very complex. ROO’s provide different functions but how they are set affords either a degree of protection or liberalisation offered to a given industry by the importing country. ROO’s are lawful international trade tools, allowed for under World Trade Organisation (WTO) terms and common practice within international trade agreements. A range of different types of ROO rules apply and more than one rule can apply to a product.

What is “cumulation”?

Ideally, inside a preferential trade agreement, countries can share production and jointly comply with the ROO provisions. This concept is known as accumulation or cumulation. As basic rules of origin set out that only products which are either produced entirely in a particular country (wholly obtained) or substantially transformed may be considered as originating in that country, cumulation is a deviation from this core concept of origin.

Manufacturing relies extensively on global supply chains characterised by component sourcing and processing being undertaken in many countries. Where two or more countries have agreed on the same ROO principles within a free trade agreement between them, if the product of one country within the agreement is further processed (substantial transformed) in another country within the agreement, the product can be considered as originating in the final country of production. The rules and determination of substantial transformation is decided on a product by product basis and will be determined by the product commodity codes assigned to each product.

Cumulation widens the definition of originating products and provides flexibility to develop economic relations between countries party to a free trade or economic relationship area.

Bilateral Cumulation

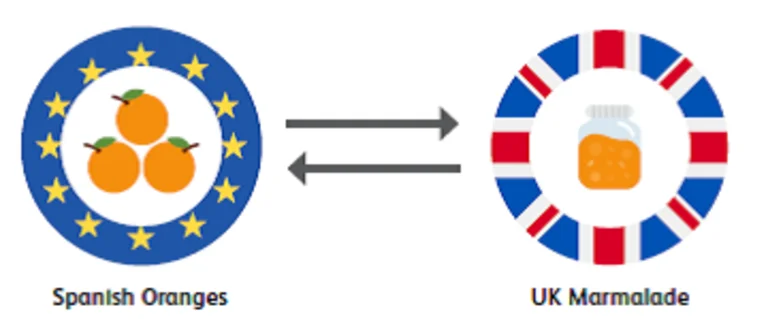

Bilateral cumulation is the most basic form and is usually between two partners where a trade arrangement allows them to cumulate origin of goods. Bilateral cumulation forms the basis of the UK-EU TCA. This means that input originating in the EU or the UK under the TCA can also be considered as originating input in the either market and therefore attracts the preferential tariff rate agreed between the UK and the EU. .

This originating status is usually supported by a proof of origin certificate that accompanies the product during the import process.

For example, in the UK-EU TCA with the same origin rules and Spanish oranges were turned into marmalade in the UK, the oranges could be considered as originating in the UK under bilateral cumulation.

In the UK-EU TCA this means products or materials originating in the EU can be considered as originating in the UK if those products are further processed in the UK or incorporated into another product prior to re-export to the EU. Under the TCA arrangements, exporters are not only able to cumulate originating materials or products, as set out above, but also processing or production carried out on non-originating materials (”full bilateral cumulation”). This means that all operations carried out in the UK or EU are taken into account when determining whether a good is able to meet a product-specific rule.

Full bilateral cumulation applies to both specific production processes (for example ‘combing’ or ‘making up’ in the manufacture of textiles products) and the value associated with such processing (for example in product-specific rules with value-add requirements).

Cumulation and insufficient production

For more information, businesses should refer insufficient production, where links to the full list of insufficient processing operations has been provided.

Claiming preferential treatment

In order for business to benefit from preferential tariffs when importing into the UK or EU, they will need to claim the preference on their customs declaration forms and declare they hold proof of origin that the goods meet the ROO.

A proof of origin is used by the importer to demonstrate that the goods qualify as originating from within the territory of the exporter and are eligible to claim preference.

UK government Guidance

Download the latest FAQ below

Requirements for Importers and Exporters

1. Have proof of the originating status of the product before claiming preference. This maybe:

- Statement on origin provided by the exporter on a commercial invoice or other commercial document that describes the goods. The text of the Statement would be included in the agreement. This is known as an invoice or origin declaration;

- Supporting documents and records if you are claiming preference using your “importers knowledge”. If using importer knowledge, you must obtain sufficient evidence that the goods qualify as originating. This may involve the exporter providing a range of supporting documentation.

If you cannot obtain that evidence, then the exporter may be able to provide a Statement on origin.

2. Claim for preference by completing the relevant part and declaring the proof of origin on your customs import declaration.

3. If requested by the customs authorities, provide the proof of origin.

4. Maintain records for at least 4 years.

1. Hold evidence that the goods meet the relevant ROO before issuing a Statement on origin.

2. Understand whether a declaration from your supplier needs to be obtained. An easement provided in the UK-EU TCA allows for businesses not to provide a supplier’s declarations when the goods are exported. This easement is in place until 31st December 2021. Businesses may be asked to retrospectively provide a supplier’s declaration, dated from 1 January 2021after this date.

3. Provide your customer, the importer, with one of the following:

- Statement on origin on a commercial invoice or other commercial document that describes the goods. The text of the Statement would be included in the agreement. This is known as an invoice or origin declaration;

Supporting documents and records if your customer is claiming preference using their “importer’s knowledge”.

4. Maintain records for at least 4 years.

Text of the Statement on Origin for the UK-EU TCA

The statement on origin referred to above shall be made out using the text set out below. If the statement on origin is handwritten, it shall be written in ink in printed characters. The statement on origin shall be made out in accordance with the respective footnotes. The footnotes do not have to be reproduced.

(Period: from___________ to __________ (1)) The exporter of the products covered by this document (Exporter Reference No ... (2)) declares that, except where otherwise clearly indicated, these products are of ... (3) preferential origin.

……………………………………………………………............................................. (4)

(Place and date)

…………………………………………………………….............................................

(Name of the exporter)

1 If the statement on origin is completed for multiple shipments of identical originating products within the meaning of point (b) of Article ORIG.19(4) [Statement on Origin] of this Agreement, indicate the period for which the statement on origin is to apply. That period shall not exceed 12 months. All importations of the product must occur within the period indicated. If a period is not applicable, the field may be left blank.

2 Indicate the reference number by which the exporter is identified. For the Union exporter, this will be the number assigned in accordance with the laws and regulations of the Union. For the United Kingdom exporter, this will be the number assigned in accordance with the laws and regulations applicable within the United Kingdom. Where the exporter has not been assigned a number, this field may be left blank.

3 Indicate the origin of the product: the United Kingdom or the Union.

4 Place and date may be omitted if the information is contained on the document itself.

For reference the text of the Statement on origin is set out in full in the UK-EU TCA (Annex ORIG-4 the TCA) here

Government Guidance

UK Global Tariff

On 1 January 2021 the UK introduced the UK Global Tariff replacing its membership of the EU Customs Union and the EU Common External Tariffs. . The UK Global Tariff applies on all eligible goods imported into the UK whether from any third country where no preferential tariff arrangement through a Free Trade Agreement has been agreed, as well as goods from the EU which do not meet ROO requirements.

Information on the UK Global Tariff schedule is available online through the gov.uk website. Information is also available on commodity codes is accessible and whether t tariffs, duty and VAT is payable and whether you are able to apply for relief.

Commodity Codes and Tariffs

DIT Trade Tariff: look up commodity codes, duty and VAT rates